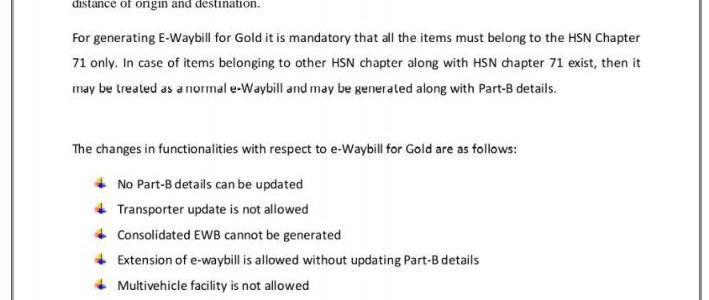

As we all are aware that the Board’s Report is prepared under subsection 3 of section 134 of the Companies Act, 2013 read with Rule 8 of the Companies (Accounts) Rules, 2014

⦁ Now, the Ministry of Corporate Affairs has amended Rule 8, after the amendment along with the existing matter contained in the Board’s Report two new matters shall be added to the Board’s Report.

⦁ The two new disclosures (along with the existing disclosures) shall be applicable for the Financial year 2021-22 and the two new disclosures are:-

Details of applications under the IBC, 2016 during the year along with their status as at the end of the financial year.

The details of the difference between the amount of the *valuation done at the time of one-time settlement and the valuation done while taking a loan from the Banks or Financial institutions along with the reasons thereof. So, you can add the above clauses in Board’s Report as follows:-

1. DETAILS OF APPLICATION MADE OR PROCEEDING PENDING UNDER INSOLVENCY AND BANKRUPTCY CODE 2016

During the year under review, there were no applications made or proceeding pending in the name of the company under the Insolvency and Bankruptcy Code, 2016

2. DETAILS OF DIFFERENCE BETWEEN VALUATION AMOUNT ON ONE-TIME SETTLEMENT AND VALUATION WHILE AVAILING LOAN FROM BANKS AND FINANCIAL INSTITUTIONS

During the year under review, there has been no time settlement of loans taken from Banks and Financial institutions

Kindly note that the above two matters shall be made in the Board’s Report only in case there is no application or proceeding pending under IBC; or where there is no loan taken or no settlement happened from the Bank.

#boardsreport #boardreport #companiesact2013 #audit #companiesaudit #statutoryaudit