In a process of Statutory Audit, the Test of Control and Test of Details are two important stages and it also makes an important question from the interview pov.

I have discussed a comparison of both gathered from my experience.

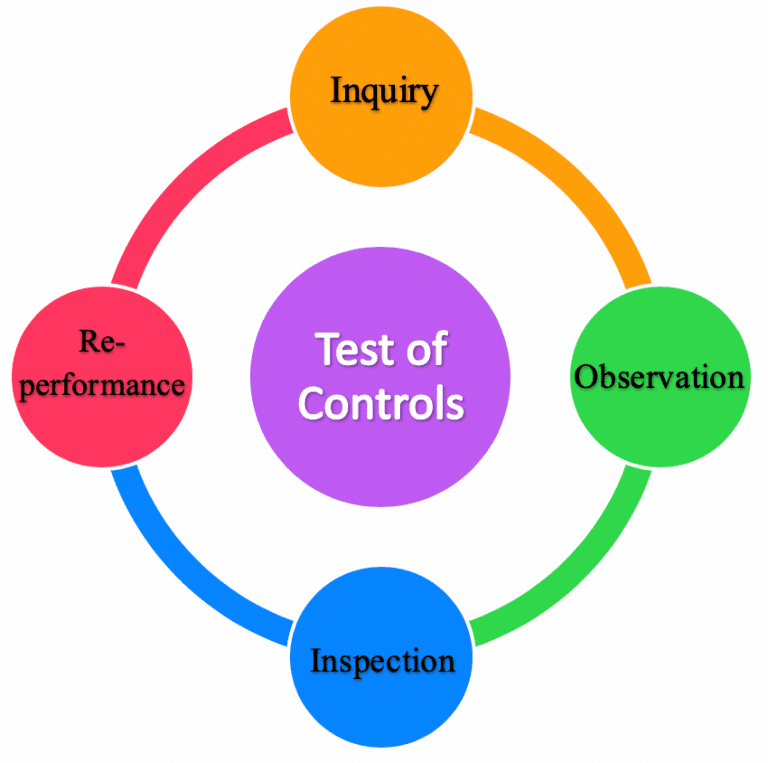

TOC is a type of audit procedure we perform to evaluate whether a client’s internal control works effectively. Thus, we perform the test to obtain evidence of effectiveness before we can rely on controls. In case controls are weak, we will need to increase our substantive tests.

So, we take out the samples from SCOT (Significant class of Transactions), test various assertions, capture the details of the given sample, and match them with supporting documents. The sample size depends on the population and frequency of control.

Based on the TOC, we determine the extent of TOD. Test of Details is a substantive procedure used to collect evidence to verify individual transactions or balances.

So, after a combined assessment of risk and control (CRA), we define the tolerable error (TE) for deviations and obtain the samples for transactions to do the testing. The goal here is to confirm that supporting docs match with each other and the source.

I have only explained the surface of it and there are a lot of other things done throughout this.

I hope it was worth a read! Do add your learnings in the comments.