Every business in India must file GST returns. Every Private Limited Company must file AOC-4 and MGT-7. Every director must complete DIR-3 KYC by September 30. These are universal compliance obligations — and almost any practicing CA can handle them.

What separates a good CA from an exceptional one — the kind that genuinely moves the needle for your business — is what they know about your industry specifically. The metrics that matter. The tax treatments that apply. The compliance traps that appear in your sector and not others. The structuring decisions that only make sense when you understand your business model.

A SaaS founder in Hinjewadi has fundamentally different financial complexity than a steel fabricator in Bhosari. An Amazon FBA seller has nothing in common with a healthcare consultancy in Baner. The GST rules, the income tax treatment, the working capital dynamics, the compliance risks — all completely different.

At Akhil Amit And Associates, we work across all of these sectors from our offices in Chinchwad, Wakad, and Ravet-Kiwale. This guide explains what industry-specific CA expertise looks like for each sector — and what it means in practice for your business.

“Generic compliance is the floor. Industry-specific financial intelligence is what actually builds your business.”

SaaS Companies — Where Revenue Recognition Meets Regulatory Complexity

Software-as-a-Service is the most financially complex business model for a CA to manage well. The revenue recognition rules are different, the GST treatment varies by customer type and location, the RCM obligations on cloud infrastructure are frequently missed, and the metrics investors care about — ARR, MRR, churn, LTV — are not standard output from an accounting system.

What a SaaS-expert CA understands that others miss

The SaaS CA Checklist — What Your CA Should Be Doing

✦ Deferred revenue accounting for annual subscriptions

✦ LUT filing before every export invoice to foreign clients

✦ RCM on AWS, Azure, Google Cloud, Zoom, GitHub

✦ OIDAR service classification for B2C international sales

✦ ARR / MRR / CAC / LTV dashboard alongside P&L

✦ Fundraising-ready financials for angel and seed rounds

✦ ESOP scheme documentation before first option grant

✦ Transfer pricing documentation for related party SaaS

Deferred revenue is one of the most mishandled accounting items for SaaS businesses in India. When a customer pays ₹1,20,000 upfront for an annual subscription, that is not ₹1,20,000 of revenue in the month of receipt. It is ₹10,000 per month recognised over twelve months. Most bookkeepers record it as full revenue immediately — which distorts your profitability, inflates your taxable income in Year 1, and depresses it in Year 2. This single error creates a tax timing mismatch that investors flag during due diligence.

Reverse Charge Mechanism on SaaS subscriptions — every AWS bill, every Google Workspace invoice, every Zoom subscription paid to a foreign vendor attracts GST under RCM. Your company — as the recipient of the imported service — must pay 18% GST to the government even though the foreign vendor does not collect it. Most SaaS founders in Pune are not doing this. It surfaces during GST audits as a significant liability.

SaaS Founders — Before Your Next Funding Round

Investors and their lawyers will check: two years of audited financials with correct revenue recognition, LUT filing history for every year you had export revenue, TDS returns with no defaults on contractor payments, and ESOP documentation if you have granted options. Building this foundation before the term sheet arrives is what separates a 72-hour due diligence from a six-week remediation exercise. See our Virtual CFO service for fundraising readiness support.

IT Companies and Technology Consultancies — Export Compliance and FEMA

Pune’s IT corridor — Hinjewadi, Kharadi, Baner, Wakad — is home to hundreds of technology companies ranging from boutique consultancies to 200-person product studios. What they share is a common set of financial complexity that generic CA advice handles badly: export GST, TDS on freelance developers, FEMA compliance when foreign clients remit payment, and the ROC compliance stack that accumulates quietly until a client relationship requires it.

The export GST mistake that costs IT companies real money

If your IT company has international clients, every invoice you raise is a zero-rated export of services — provided you have filed a Letter of Undertaking (LUT) before the first invoice of each financial year. The LUT is not automatic, is not part of GST registration, and must be filed fresh every April 1.

Without a filed LUT, every export invoice either attracts 18% GST (which your foreign client will refuse) or creates a liability you must pay and later claim as a refund — which is slow, cash-flow negative, and entirely avoidable. We have seen IT companies in Hinjewadi running two years of export revenue without ever filing the LUT.

For a detailed breakdown of IT-specific compliance — including TDS on freelance developers, RCM on cloud subscriptions, and ESOP structuring for growing tech teams — see our comprehensive guide on CA services for IT companies and startups in Pune.

invoice without LUT

developer payments

if missed at start

Manufacturing and Engineering — Costing, Inventory, and Working Capital

Pimpri Chinchwad, Bhosari, and Chakan constitute one of the largest manufacturing clusters in India — automotive components, precision engineering, plastics, food processing, chemicals, and heavy fabrication. The financial complexity of a manufacturing business is fundamentally different from a service business: inventory valuation methods directly affect taxable income, job costing determines whether individual production runs are profitable, and working capital structuring determines whether the business can fund its own growth.

The three financial decisions that separate profitable manufacturers from margin-squeezed ones

Manufacturing CA Expertise — What We Do Differently

Job Costing and Product-Level Profitability

Most manufacturing P&Ls show aggregate profit. Job costing breaks it down by product line, client, or production run — telling you which orders are worth taking and which are silently eroding margin. Without this, manufacturers grow revenue and shrink margin simultaneously.

Inventory Valuation Method Selection

Weighted average cost, FIFO, and specific identification produce different taxable income in different market conditions. In a rising raw material cost environment, the method chosen affects tax outflow directly. This is a structural decision made once — and changed only with difficulty.

MSME Payment Protection and Working Capital

Registered MSME manufacturers have a statutory right to payment within 45 days from corporate buyers. Buyers who pay beyond 45 days must pay compound interest from the agreement date. Most Bhosari and Chakan manufacturers are not enforcing this — leaving crores of interest unclaimed annually.

GST Input Tax Credit for manufacturers is both an opportunity and a risk. The ITC chain — from raw material supplier through production to final sale — must be documented precisely. Credit mismatches flagged in GSTR-2A reconciliation translate directly into demands. A manufacturing-focused CA audits the ITC position monthly, not just at annual return time.

Working capital financing for manufacturing businesses — bill discounting, channel financing, CGTMSE loans, and Udyam-linked credit facilities — requires clean financial statements and an auditor who can speak the language of industrial banking. Manufacturers with well-maintained books access credit at significantly better terms than those with reactive compliance.

“A manufacturer who knows their product-level margin makes fundamentally different decisions than one who only knows their aggregate profit. This is what job costing gives you.”

Amazon FBA and E-Commerce — The Most Misunderstood Tax Situation in Indian Business

Amazon FBA sellers and e-commerce brands running on Flipkart, Meesho, Myntra, or their own Shopify store have a tax situation that most CAs in India have never encountered in practice. The GST rules for marketplace-based selling are distinct from everything else. The TCS deducted by Amazon is different from TDS. Multi-state inventory creates phantom tax liabilities. Return transactions reverse GST in ways that most accounting software handles incorrectly. And the reconciliation between Amazon’s settlement reports and your books is a process that demands attention every single month.

The five Amazon FBA compliance gaps we fix every time

Gap 1 — TCS vs TDS Confusion

Amazon India deducts Tax Collected at Source (TCS) at 1% on every payment to sellers under Section 52 of the GST Act. This is not TDS under Income Tax. It must be claimed as credit in your GSTR-3B every month by reconciling your Amazon seller account with your GST returns. Most Amazon sellers either do not claim it (losing real cash) or confuse it with income tax TDS (filing incorrectly).

Gap 2 — Multi-State Inventory and Place of Supply

Amazon FBA sellers who use Amazon’s fulfilment centres across multiple states — Mumbai, Delhi, Bengaluru, Hyderabad — have inventory in multiple states. When a product ships from a fulfilment centre in a different state than your registration, GST rules around consignment stock, branch transfers, and place of supply apply. Many sellers pay incorrect GST for years without realising.

Gap 3 — Return and Refund GST Treatment

Product returns on Amazon reverse the original transaction. The GST implication depends on whether the return happens within the same month as the original sale (credit note in the same period) or in a subsequent month (time-of-supply rules apply differently). Most accounting software for Amazon sellers handles this incorrectly by default, creating a running GST mismatch that builds over years.

Gap 4 — Settlement Reconciliation

Amazon pays sellers every two weeks via settlements that net out sales, returns, fees, and FBA charges. The settlement amount is not your revenue — it is a net figure after multiple deductions. Revenue must be grossed up, Amazon fees must be accounted as expenses, and the reconciliation must match your GSTR-1 sales declaration. This monthly reconciliation is non-negotiable for accurate GST filings.

Gap 5 — Unit Economics and Profitability by SKU

Amazon’s fee structure — referral fees, FBA fulfilment fees, storage fees, advertising costs — must be assigned at the product level to understand real margin. A product with 40% gross margin can be loss-making after Amazon fees and advertising. A CA who builds a unit economics model for your catalogue tells you which ASINs to scale and which to kill. Without this, sellers scale unprofitable products.

Service Sector Businesses — Retainer Economics, TDS Web, and Professional Tax

The service sector in Pune is enormous and diverse — management consultancies, marketing agencies, legal firms, HR and recruitment businesses, training companies, architects, designers, financial advisors. What they share is a common financial structure: service-based revenue, low tangible assets, high dependence on professional talent, and a TDS web that runs in both directions — clients deduct TDS from payments to you, and you must deduct TDS from payments to your contractors and vendors.

Managing the two-directional TDS position

Service businesses simultaneously sit on both sides of TDS. Large corporate clients deduct TDS at 10% under Section 194J from payments to your firm — which creates a TDS credit that you claim when filing your income tax return. Simultaneously, you must deduct TDS from payments to your own vendors, contractors, freelancers, and subcontractors.

The TDS that clients deduct from you must be matched against your 26AS / AIS statement precisely. Mismatches in your 26AS — where a client deducted TDS but never deposited it or filed with a wrong PAN — are your problem to resolve, not theirs. A CA who manages this reconciliation quarterly prevents the cascading issue of unrecoverable TDS credits.

| Service Business Type | Key GST Treatment | Critical TDS Section |

|---|---|---|

| Management Consulting | 18% GST on all fees | 194J — 10% from corporate clients |

| Digital Marketing Agency | 18% GST; platform ad spend handling | 194J on agency fees; RCM on Meta/Google ads |

| Recruitment / HR | 18% GST on placement fee | 194J / 194H depending on structure |

| Architecture / Design | 18% GST; works contract where construction involved | 194J on professional fees |

| Training and EdTech | 18% GST; exemptions for recognised education | 194J on faculty / content payments |

Retainer vs project billing creates different GST time-of-supply implications. A monthly retainer creates a GST liability on the invoice date every month. A project completion billing creates liability at delivery. When retainers are paid in advance, the advance itself creates a GST point of supply. Managing this correctly — especially for service businesses with mixed billing models — requires ongoing attention, not annual clean-up.

The Compliance Foundation Every Business Shares

Regardless of sector — SaaS, IT, manufacturing, Amazon, or services — every Private Limited Company in Pune has the same core compliance obligations. Industry expertise is built on top of this foundation, not instead of it.

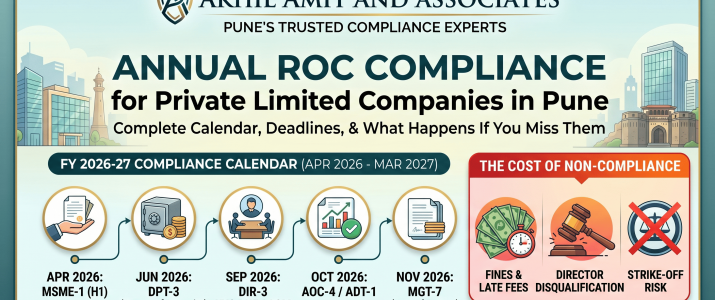

The annual ROC compliance calendar — INC-20A, ADT-1, DIR-3 KYC, AOC-4, MGT-7 — applies equally to a SaaS startup in Baner and a steel fabricator in Chakan. Missing any of these deadlines compounds penalties daily. The formation decisions made at incorporation — MOA object clause, authorised capital structure, share certificate documentation — affect every sector equally.

What changes by sector is the layer above the foundation: how revenue is recognised, how GST applies to the specific supply type, how working capital is structured, and what financial intelligence is relevant to the business decisions you are making.

Frequently Asked Questions

Does my SaaS company need to register for GST in Pune if all revenue is from foreign clients?

Yes. A SaaS company providing services to foreign clients is making exports of services — but GST registration is still mandatory from the first transaction, because you must file LUTs and claim ITC on your input services. Without registration, you cannot file the LUT that enables zero-rated exports. For complete GST guidance, see our GST registration page.

I am an Amazon FBA seller. Do I need to register in multiple states?

If Amazon stores your inventory in fulfilment centres in states other than Maharashtra, you technically have a business presence in those states and should evaluate multi-state GST registration. The threshold for mandatory registration changes once there is a fixed establishment (like an Amazon FC holding your stock). This analysis is specific to your SKU mix and the FCs Amazon assigns — contact us on +91 8918900780 for a specific assessment.

What is the difference between a CA who works with manufacturing businesses and a general CA?

A manufacturing-specialist CA implements job costing systems, advises on inventory valuation methods that optimise tax position, manages GST ITC reconciliation at the input level, and understands the MSME payment protection framework. A general CA files returns correctly but cannot advise on these operational and structural questions. For manufacturing businesses in Bhosari, Chakan, and PCMC, the difference shows up directly on the P&L over time.

How does Akhil Amit And Associates serve so many different sectors from Pune?

We have built a team with specialised knowledge across sectors — including CA professionals with experience in IT/SaaS compliance, manufacturing finance, e-commerce taxation, and service sector advisory. Our three offices in Chinchwad, Wakad, and Ravet serve different industry clusters across Pune and Pimpri Chinchwad. We currently manage compliance for 250+ companies with 1,500+ clients served across these sectors. See our full FAQ page for more.

Can you help with Virtual CFO services for a growing service business?

Yes. Our Virtual CFO service is designed for businesses across all sectors that have outgrown basic bookkeeping but are not yet ready for a full-time CFO hire. This includes service businesses building MIS dashboards, manufacturers needing cash flow forecasting, and SaaS companies preparing for fundraising.

Related Guides on This Blog

→ CA for IT Companies and Startups in Pune — Complete Compliance Guide

→ Private Limited Company Registration — The Premium Founder’s Playbook

→ Annual ROC Compliance Calendar — Every Deadline, Every Penalty

→ Post-Incorporation Registrations — GST, Shop Act, Udyam and Profession Tax

→ Frequently Asked Questions — Company Registration and Compliance